Crudely Optimising an Oil Refinery

This article scratches the surface of how oil is used and traded within the world’s energy complex. We introduce linear optimisation utilising AMPL to understand the optimal outputs from a fictitious refinery.

Macroeconomics with Gaussian Mixture Models

Returns can be viewed as a product of an underlying market regime. This article models those regimes and shows how to extend the model with macroeconomic variables to link regimes to observable economic indicators.

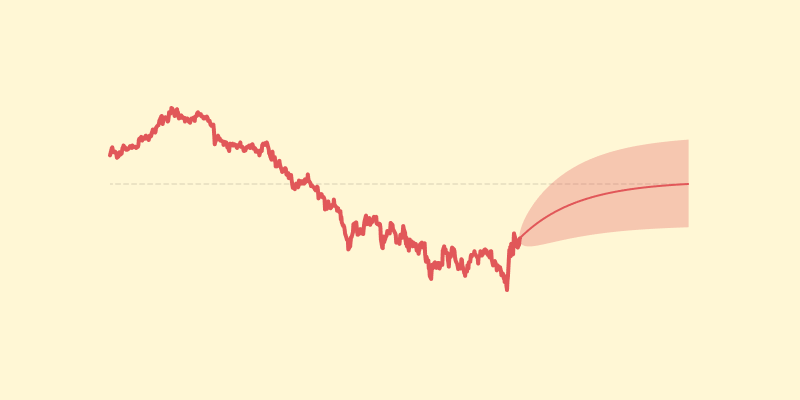

Conditional Value at Risk

A practical crash course on conditional value at risk. Why it beats value at risk, how to estimate it from real data, and how to optimise portfolios with it. Complete with working code.

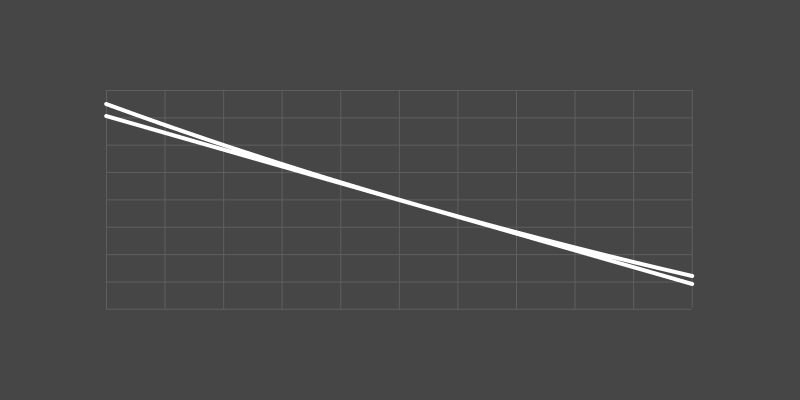

Modelling the yield curve of US government treasuries

I show you how to build a factor model of US treasury yields. The factor model captures fundamental features of the whole yield curve.

Key insights: Imbalance in the order book

I summarise key insights from a few papers studying the limit order book. You’l learn how to measure volume imblanace in the limit order book and how well it predicts price moves.

Forecasting currency rates with fractional brownian motion

Fractional Brownian motion is a stochastic process that can model mean reversion. Predicting future values turns out to be a simple linear model. This model has significant predictive power when applied to currencies.

Mean reversion in government bonds

Using the Ornstein–Uhlenbeck process, you can calculate the expected spread between bond yields of different maturities. These expected values can then be used to estimated the expected value of treasury ETF spreads.

Calculating the mean and variance of bond returns

Bond returns are a function of yields. Calculating the expected value of this function is quite difficult. You can take a Taylor expansion to make calculating the mean and variance of returns much easier.

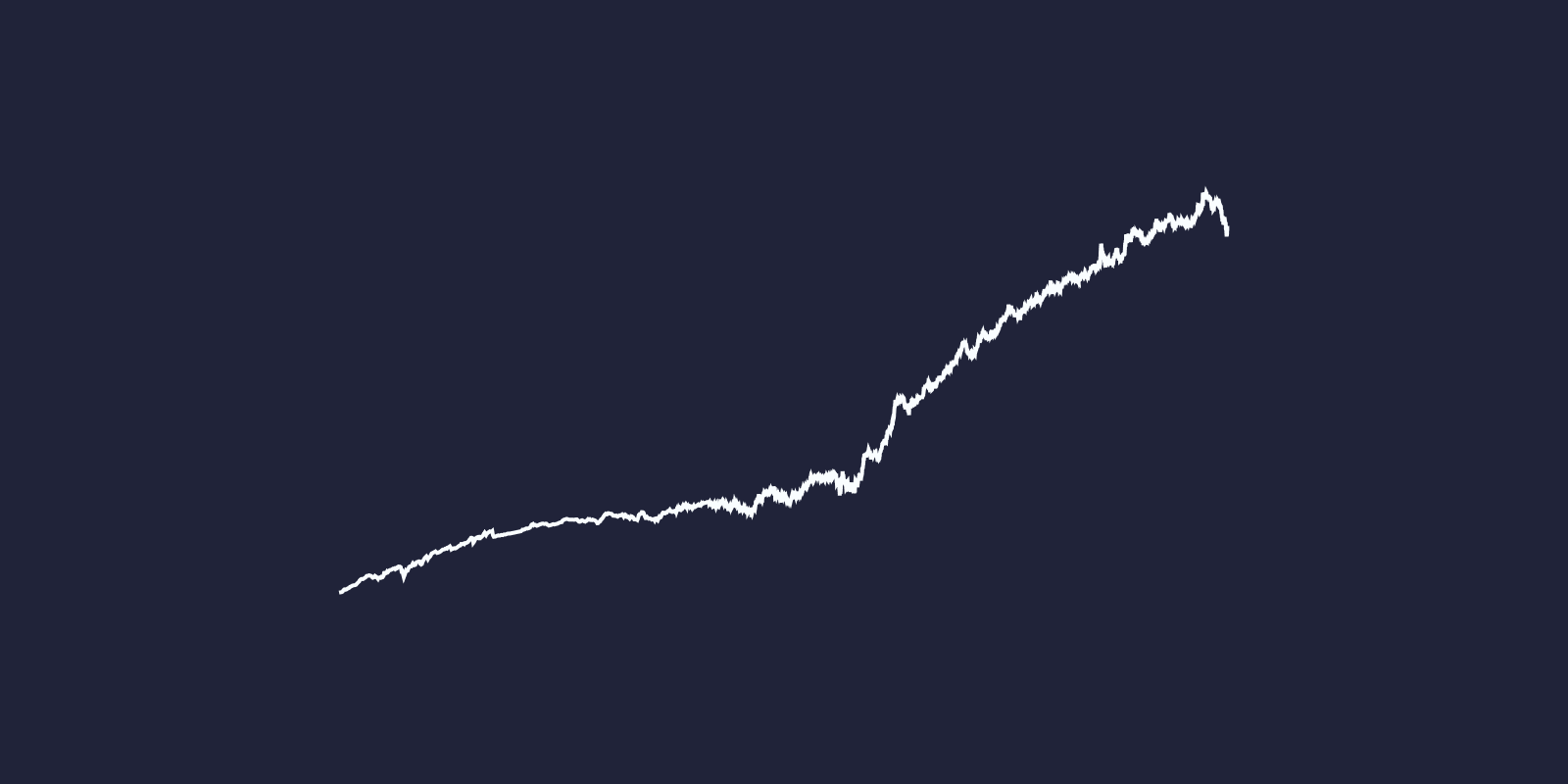

How to get 100 years of bond ETF prices

The price of a bond ETF can be estimated from bond yields. You can use this technique to create a long term performance history of an ETF.

Understanding bond ETF returns

The return of a bond ETF can be estimated from bond yields. The distribution of a bond ETF’s returns turns out to be a function of the interest rate, expected change and variance of the interest rate. Bond returns are skewed depending on the interest rate’s level.

Invest regularly

Successful investors combine lots of simple things, each one providing a small improvement. One of these simple things is investing regularly.

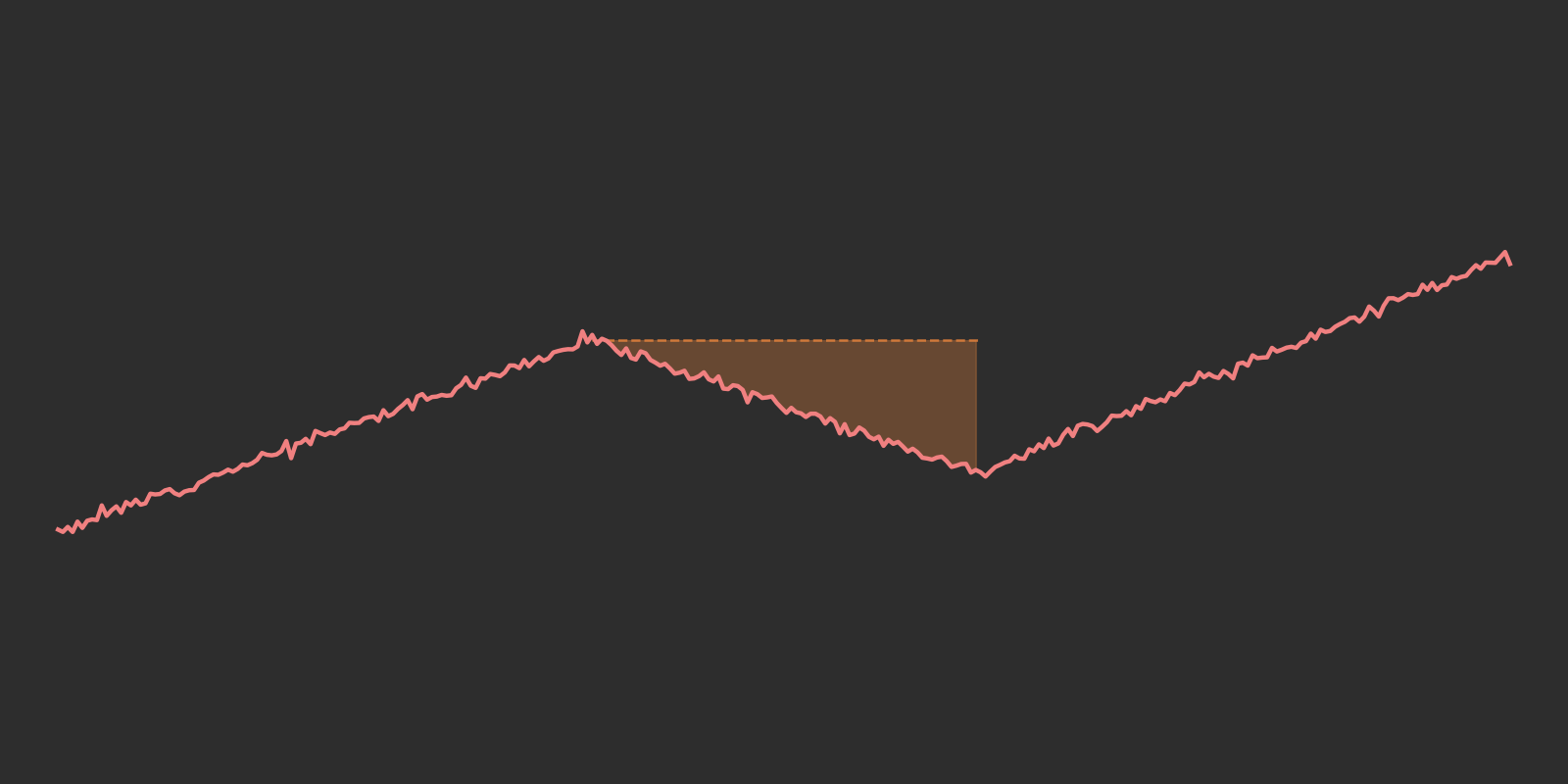

Measuring performance

How can you measure performance when investing? You might think you can simply measure how much money you make. However, this can lead to losing a large portion of your capital. I want to show you why that can happen and how I measure my own investment performance.